The EUR/USD pair maintained its advance during the first part of the week, but failed spectacularly at parity, finishing the week at about 0.9750, resulting in a slight weekly loss.

Optimism reigned supreme at the start of the fourth quarter, with Wall Street reporting massive gains and government bonds extending their gains from the previous week.

Market participants believed that the growing likelihood of a worldwide recession would push central banks to decrease the pace of quantitative tightening sooner rather than later.

The Reserve Bank of Australia raised the cash rate by 25 basis points, which was less than expected, feeding such speculation as well as demand for high-yielding assets.

But the good vibes didn't last long. The common currency began losing value on Wednesday, as the EU proposed more sanctions on Russia for its February invasion of Ukraine.

Sanctions were imposed following the unlawful annexation of the regions of Donetsk, Luhansk, Kherson, and Zaporizhzhia, and included a price ceiling on Russian oil as well as restrictions on imports and exports from and to the nation.

Furthermore, sluggish EU statistics rekindled fears of an economic downturn in the Union, dampening the risk-positive mood. S&P Global revised its September PMIs lower, indicating a worse decline in the business sector.

At the same time, wholesale inflation in the EU rose by 43.3% year on year in August, but retail sales in the same month declined by 0.3%, while German sales fell by 1.3%.

The European Central Bank Monetary Policy Meeting Accounts also had an impact on the common currency. According to the memo, some officials favored a larger rate rise of 50 basis points.

Furthermore, the median three-year inflation projection remained at 3%. Policymakers emphasized that the devaluation of the euro might worsen inflationary pressures, but that acting "decisively" now will obviate the need to hike more aggressively later.

Market mood deteriorated further as speakers from the US Federal Reserve hit the wires, echoing their well-known hawkish tone.

Minneapolis Fed President Neel Kashkari stated that there is more work to be done on inflation, and that while there is a danger of overshooting, there is essentially no indication that inflation has peaked.

The Federal Reserve Bank of Chicago's Charles L. Evans and Cleveland Federal Reserve Bank President Loretta Mester have stated that inflation is their main focus.

Finally, Governor Christopher Waller stated that he sees no cause to slow the Fed's policy tightening. Meanwhile, data from the United States has fueled expectations that the Federal Reserve would continue on its aggressive monetary tightening course.

According to the September Nonfarm Payrolls data, the country added 265K new positions in September, which was more than expected but lower than the prior month.

Unemployment fell unexpectedly to 3.5%, but labor-force participation fell less than predicted to 62.3% from 62.4% in August. The news followed a string of dismal US employment numbers.

Market participants heard on Tuesday that the number of job opportunities fell dramatically in August, while layoffs and discharges remained over 1.5 million.

Furthermore, according to the Challenger Job Cuts report issued on Thursday, US-based firms reported 29,989 layoffs in September, up 46.4% from August and 67.7% from a year earlier.

Finally, initial jobless claims for the week ending September 30 surged unexpectedly to 219K, above the 200K forecasts. Despite mixed data, the job sector appears to be robust enough to withstand rate increases.It all comes down to inflation.

The ensuing week will include fewer but more exciting events. On Wednesday, the US Federal Reserve will issue the Minutes of its most recent meeting, and on Thursday, the government will release the September Consumer Price Index.

Annual inflation is expected to rise by 8.1% this year, slightly higher than the previous 8.3%. The core reading is expected to be 6.5%. If the CPI fell in August, it will likely have little influence on what the market anticipates the Fed will do.

Germany will publish the September Harmonized Consumer Price Index, which is predicted to remain at 10.9%. Finally, the spotlight will be on US September Retail Sales on Friday.

The EUR/USD pair temporarily traded above the 61.8% Fibonacci retracement of the 1.0197/0.0535 drop at 0.9945, but it ended the week below the 38.2% retracement at 0.9790, suggesting that the corrective rise may have ended.

In the next days, the pair might retest and potentially break below the lower end of the range.The weekly chart reveals that the pair also failed just ahead of the daily falling trend line from the year high at 1.1494, indicating that the bearish trend will continue in the near future.

The 20 SMA remains well above the trend line and considerably below the lengthier ones. Meanwhile, technical indicators continue to show a lack of directional strength at oversold levels.

The risk is weighted to the downside on a daily basis. The pair is trading below all of its moving averages, which are all pointing south. Meanwhile, technical indicators maintain their downward trend after failing to break through their midpoints.

At about 0.9690, the 23.6% retracement of the aforementioned daily decline provides immediate support. The 0.9600 level is the next to monitor, ahead of the multi-year low of 0.9535.

Sellers will most likely wait for parity between 0.9870 and 0.9945. Even if the pair recovers above the latter, it must clear the trend line at approximately 1.0050 to avoid falling.

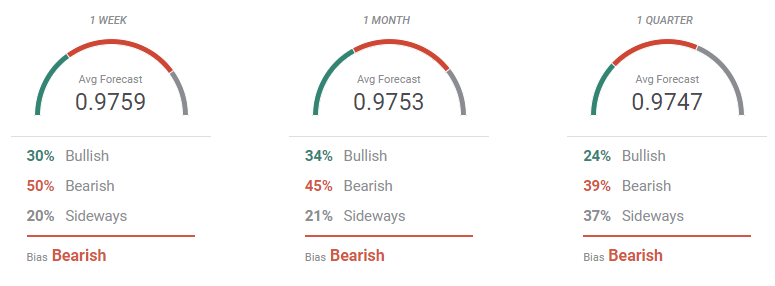

According to the FXStreet Forecast Poll, the EUR/USD will likely stay under selling pressure in the next weeks. Bears dominate all time frames under consideration. From now through the end of the year, the pair is expected to remain steady around the 0.97 range.

The EUR is shown in a bleak light in the Overview chart. The three moving averages continue to fall, repeating their falls and setting new annual lows.

More importantly, the monthly and quarterly perspectives suggest that a growing percentage of market players are now forecasting lower lows for the year below 0.9500, with probable falls below 0.9000.

|

HOT TOPICS |

|

|

|

|

Brief Market Analysis For 2022 For Global Futures Trading Platforms |

|